The Energy Policy magazine published an article by Alexey Belogoryev on the future gas demand prospects in China.

High growth rates of natural gas consumption are expected in the coming years in China. According to our estimates, the average annual increase until 2030 will be about 4.5%. In total, by 2030, in the baseline scenario, consumption may increase to 520-530 billion cubic meters per year compared to 390 in 2023. Higher estimates (up to 600 billion cubic meters) can still be found in the expert environment, but such optimism, in our opinion, looks less justified. In any case, the rapid growth in demand, noticeably outstripping the increase in domestic production, creates favorable conditions for increasing exports of Russian pipeline and liquefied natural gas to China. But how much of this gas will China need?

Fig. 1. The share of natural gas in primary energy consumption in 2023. Sources: FIEF according to The Energy Institute, BP

Why is the demand growing?

In recent years (excluding 2022), the growth rate of gas consumption in China has decreased for all major consumer groups, but remains high. In 2019-2021, the average annual growth was 10.2%. By industry, the fastest growth rates are shown by industry (+12% in 2019-2021), as well as electric power and heat supply (+10%).

The heterogeneous dynamics of consumption is due to government policy aimed at primarily replacing coal with gas in industry in the absence of significant measures to stimulate the development of gas power generation.

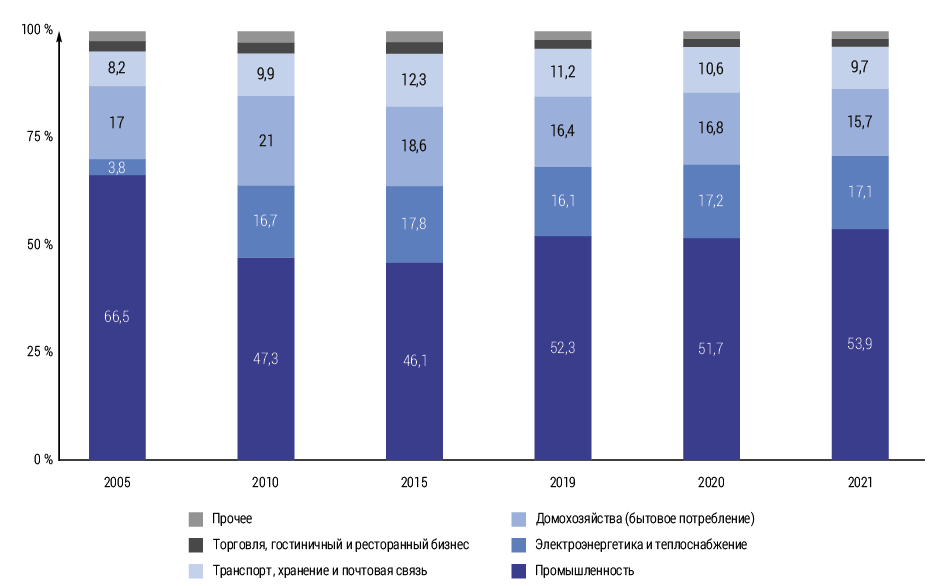

Fig. 2. The structure of gas consumption in China. Source: FIEF according to the National Statistical Bureau of the People's Republic of China

Therefore, it is not surprising that the main driver of gas demand growth in China, unlike many other developing countries, has traditionally been industry. In 2019-2021, it accounted for 61% (+58 billion cubic meters) of the total increase in demand. Gas consumption in industry (excluding the production and distribution of electricity and heat) still reaches 54% of total gas consumption in China. The structure of industrial consumption is dominated by the manufacturing industry (73% in 2021), and within it – the chemical industry (40%), metallurgy (20%), oil refining, coal, etc. (12%), mechanical engineering (11%). The largest increase in consumption has been observed in recent years in the chemical industry. Also, an increase in demand is observed in the agro-industrial complex, metallurgy, pulp and paper industry and mechanical engineering.

Fig. 3. The change in monthly electricity generation in China by generation types compared to the same period of the previous year. Source: FIEF according to Ember

The share of the electric power industry in gas consumption has stabilized in recent years at the level of 16-17%. Gas power generation in China remains uncompetitive in price compared to coal due to the disparity in domestic prices for these energy resources. The choice in favor of gas is most often due not to economic incentives, but to the political objectives of regional authorities and enterprises to reduce emissions of pollutants.

In 2023 electricity production at gas-fired thermal power plants has increased to 285 billion kWh (+6.4% YoY), but its growth rate is chronically lagging behind total electricity generation, so the share of gas in it has been decreasing in recent years, still barely reaching 3% of total generation.

In 2023, gas-fired thermal power plants accounted for only 2.8% of the total increase in electricity production. Almost all of the increase is provided by coal, wind and solar generation.

The share of households in consumption gas is gradually decreasing, despite the rapid increase in the number of urban household consumers. In 2022, 49.6% of China's urban population, or 457 million people, consumed gas.

A distinctive feature of China is the high share of transport in gas consumption (10-11%) due to the large-scale development of the gas engine fuel market, not only CNG, but also LNG.

Gas imports

Gas imports to China increased in 2023 to 166 billion cubic meters (+10% YoY), of which 59.4% is LNG and 40.6% is pipeline gas. In January-May 2024, gas imports increased by 17.4% YoY or 9% compared to the same period in 2021.

Gas production and balance in China until 2030

The gap between domestic consumption and China's own natural gas production is steadily increasing, and this trend will continue at least until the early to mid–2030s. But despite lagging behind demand, gas production is growing at an impressive pace, and this trend is also stable. In 2023, it increased to 230 billion cubic meters per year (+5.5% YoY), prematurely reaching the target of the 14th five-year plan, scheduled for 2025. By 2025-2026, production is expected to increase to 260 billion cubic meters, by 2030 – to 300 billion cubic meters.

What will happen after 2030?

The Chinese gas market is far from saturated, its gas intensity will continue to grow until 2030, and the peak in demand will probably be passed no earlier than 2035 or later. According to our assessment, the Chinese authorities will strive to further restrain the growth of the gas imports share in its consumption within 40%, in the worst case – 50% (from 2018 it ranges from 40-43%), including taking into account the negative experience of the European gas crisis in 2022. This puts gas consumption in strict dependence on the rate of increase in domestic production, which remains quite uncertain after 2030. The limit of production growth, according to current estimates (FSEG, REA, etc.), may be 430-450 billion cubic meters per year, taking into account the increase in the production of so-called low-carbon gases: biomethane, hydrogen, low-carbon synthesis gas, etc. But such an indicator will be possible to achieve only by 2050.

After 2030, the gas consumption growth rates are expected to decrease more sharply than in 2024-2030 and demand will peak in the period 2035-2040. We believe that peak consumption will not exceed 600 billion cubic meters per year. By this time, domestic gas production will amount to about 320 billion cubic meters per year, which means an increase in imports by no more than 40 billion cubic meters per year by 2030. Gas imports to China will most likely reach their peak in the period from the late 2020s to the early 2040s at the level of 230-280 billion cubic meters per year.

Export prospects from Russia

In 2023, Russian pipeline gas supplies to China via the Power of Siberia gas pipeline reached 22.7 billion cubic meters. In 2024, they will amount to about 30 billion cubic meters, and in 2025 they will probably reach the design level of 38 billion cubic meters per year. Starting from 2028-2029, after the expected launch of the Far Eastern Route from Primorsky Krai in 2027, supplies should reach the current contracted volume of 48 billion cubic meters per year. Russia can also help Uzbekistan and Kazakhstan, which are experiencing increasing problems with the gas balance, in fulfilling their contractual obligations to the PRC. But most likely, Russian participation will not be direct, but indirect – through exchange operations, i.e. formally, Russian gas will be used to supply domestic markets of Central Asian countries. According to our estimates, the value of such swaps may reach 8-9 billion cubic meters per year in the future.

Commercial deliveries via the Power of Siberia 2 gas pipeline may begin no earlier than 2030-2032, and reaching full capacity is possible at best by 2034-2035. But the project may be postponed to a later date. From China's point of view, the main disadvantage of the project is the need to provide long-term guarantees of demand for such a large volume of gas (50 billion cubic meters per year) against the background of high uncertainty of the PRC's gas balance after 2030. As we have already noted, in the baseline scenario, the entire increase in gas imports to China in the 2030s may amount to only 40 billion cubic meters.

The main uncertainty in assessing Russian gas supplies to China until 2030 is related to the volume of the expected swap with Kazakhstan and Uzbekistan, as well as the scale of additional LNG supplies beyond the long-term contracts already concluded, including from the Arctic LNG 2 and Baltic LNG plants under construction and the planned Murmansk LNG and Ob LNG, if the latter are put into operation before 2030.

The total export of Russian gas to China by 2030 can be estimated at 84 billion cubic meters per year, of which 67% (as in 2023) should be provided by pipeline supplies, including swap through Kazakhstan. According to our assessment, these volumes are provided with guaranteed demand in China, provided they are price competitive and able to circumvent the sanctions restrictions imposed by the United States and the EU.

Subscribe for updates

and be the first to know about new publications